I Bonds have increased significantly over the past two years, making them a savings product worth paying attention to once again. Fully-backed by the U.S. government, I Bonds are considered extremely safe and could be a good choice for many savers.

Never heard of an I Bond before? You’re not alone. They haven’t been popular for the last 20 years, but I’ll explain why they’ve recently become a hot trend.

However, you should strongly consider saving money in a high-yield savings account since many banks have been raising their rates. For example, the SoFi Savings Account is providing an excellent rate of 4.30% APY (with a $325 welcome bonus!) without the time restrictions of I Bonds.

This post may contain affiliate links, meaning I get a commission at no cost to you if you decide to make a purchase through my links. Visit this page for more information. The content on this page is accurate as of the posting date; however, some of the offers mentioned may have expired.

I Bonds Overview

Inflation seems to be everywhere these days. Soaring gas prices, sky-high construction costs, and expensive Uber rides. There’s definitely a lot to complain about!

But complaining doesn’t get you anywhere. Instead, consider how to make money as inflation heats up with I Bonds.

What are I Bonds?

I Bonds, short for Series I Savings Bonds, are inflation-indexed U.S. savings bonds. It’s designed to protect the value of your cash from inflation.

I Bonds are a unique, very low-risk investment backed by the U.S. Treasury with a holding period from 12 months to 30 years. Think of Series I Bonds as bank certificate of deposits (CDs) that are liquid after 12 months.

You can’t redeem an I Bond within the first 12 months and if you cash it out before five years have passed, you’ll incur three months’ worth of interest as an early withdrawal penalty.

It earns a composite rate; one rate is a fixed interest rate determined at the time you buy an I Bond and the other rate is a variable rate that gets adjusted for inflation every six months. Combine the rates together and you get the composite rate (which is the total rate you earn interest on).

The variable rate essentially guarantees I Bond buyers that they’ll never lose the value of their money because of inflation.

I know, I know – this isn’t as thrilling as showing off all the money you’ve made from bank bonuses, but you’ll make a great deal more money now with Series I Bonds than parking your cash in a traditional savings account.

I Bond Benefits

Keep in mind that I Bonds have special benefits compared to other savings products (savings account, money market account, or CD), including:

- Exemption from state income taxes

- Redemption for higher education is exempt from federal taxes

- Tax deferral until bond redemption

- Inflation protection

These are things you should consider besides the actual rate the bonds provide.

Why didn’t you recommend I Bonds before?

Because I Bonds haven’t been relevant for 20+ years. Inflation has been so low for the past couple of decades that there were better places to safely invest your cash for a higher return.

When I Bonds first came out in 1999, they were offering an impressive 7% composite rate. Since then, I Bonds rates have sunk to the bottom of the ocean floor with a fixed interest rate of 0% and a mediocre variable rate.

However, variable rates have shot up recently due to high inflation and that’s what everyone’s excited about! Here are the historical rates of I Bonds for the previous few years along with its variable inflation rates:

| Issue Date | Fixed Rate | Variable Rate | Composite Rate |

| May ’25 – Oct ’25 | 1.10% | 1.43% | 3.98% |

| Nov’24 – Apr ’25 | 1.20% | 0.95% | 3.11% |

| May ’24 – Oct ’24 | 1.30% | 1.48% | 4.28% |

| Nov ’23 – Apr ’24 | 1.30% | 1.97% | 5.27% |

| May ’23 – Oct ’23 | 0.90% | 1.69% | 4.30% |

| Nov ’22 – Apr ’23 | 0.40% | 3.24% | 6.89% |

| May ’22 – Oct ’22 | 0.00% | 4.81% | 9.62% |

| Nov ’21 – Apr ’22 | 0.00% | 3.56% | 7.12% |

| May ’21 – Oct ’21 | 0.00% | 1.77% | 3.54% |

| Nov ’20 – Apr ’21 | 0.00% | 0.84% | 1.68% |

| May ’20 – Oct ’20 | 0.00% | 0.53% | 1.06% |

| Nov ’19 – Apr ’20 | 0.20% | 1.01% | 2.22% |

| May ’19 – Oct ’19 | 0.50% | 0.70% | 1.90% |

How To Calculate I Bonds Rates

Inflation numbers released at BLS.gov helps us calculate what I Bonds rates will be. As time gets closer to the next rate adjustment, our prediction is more accurate because we have more months of inflation data to use in the calculation.

I say predict because we can only calculate what the variable inflation rate will be, and not the fixed interest rate. Remember that the total interest offered is a composite of the two rates.

Fixed Rate

The fixed rate formula is unknown, but it’s linked to the yield of short-term Treasure Inflation-Protected Securities (TIPS). Short-term TIPS are hovering just over 1% and therefore the fixed interest rate for I Bonds will likely stay close to ~1%.

The fixed rate was as high as 3.60% back in May 2000. Those lucky I Bond holders would now earn an incredible 7.54% for the six months starting in November 2023 (3.60% fixed + 3.94% variable).

Every six months, your I Bonds rates will adjust. The fixed rate will always stay at the same rate at the time of your purchase, while the variable rate will be based on inflation changes.

The fixed rate for I Bonds purchased after April 2025 is 1.10%.

Variable Rate (Inflation Rate)

The variable rate, or inflation rate, is determined by how much inflation has gone up or down in the most recent six-month period.

I Bonds uses the Consumer Price Index for Urban Consumers, or CPI-U for short, which measures the overall change in consumer prices based on a representative basket of goods and services over time (e.g. housing, apparel, transportation, food, medical care, etc).

The variable rate for I Bonds purchased after April 2025 is 1.43%.

Composite Rate

The composite rate is the combination of the fixed rate and variable rate, and is the total rate earned from I Bonds.

The formula below shows you how to calculate the composite rate. As you can see, it’s not quite as simple as adding the two rates together:

Composite Rate = Fixed Rate + 2 x Semiannual Inflation Rate + (Semiannual Inflation Rate x Fixed Rate)

I’ll walk through how to use this formula for I Bonds purchased between May 2025 to October 2025.

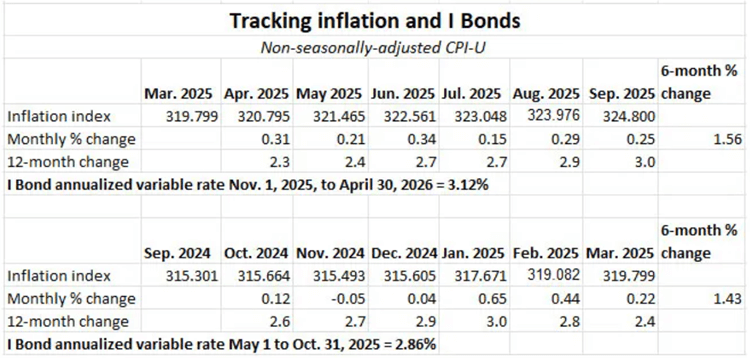

May 2025 – October 2025 I Bond Rates

The CPI-U was 315.664 in September 2024 compared to a CPI-U of 319.799 in March 2025. To determine the percentage of increase, you subtract the new number from the old number: 319.799 – 315.301 = 4.498

Next, divide this by the old CPI-U reading: 4.135 divided by 315.664 = 0.01426.

You then multiply that number by 100: 0.01426 x 100 = 1.426 or 1.43%, which is the semi-annual inflation rate. This represents a 1.43% increase.

Let’s plug these numbers into the formula I mentioned a minute go:

Total Rate = Fixed Rate + 2 x Semiannual Inflation Rate + (Semiannual Inflation Rate x Fixed Rate)

Total Rate = 0.012 + 2 x 0.0143 + (0.0143 x 0.012)

Total Rate = 4.08%

I Bonds purchased between May 1, 2025 and October 30, 2025 will earn a rate of 4.08% for the first six months of ownership. The composite rate will then adjust every six months based on inflation.

Earning 4.08% is a solid return, but it’s far less than what I Bond rates were recently. The rate was as high as 9.62% during the period of May 2022 to October 2022, and 6.89% during the the period of November 2022 to April 2023. At those rates, you were enjoying stock market like gains with zero risk.

November 2025 – April 2026 I Bond Rates

Now that we’ve established purchasing I Bonds between November 2024 and April 2025 will earn a guaranteed 4.08% return for the first six months of ownership, you may be wondering what you’d earn after the initial six months.

Well, we know that March 2025 CPI-U was 319.799 and September 2025 CPI-U is 324.800. Calculating the difference in those six months, this represents a 1.56% increase.

The fixed interest rate is currently 1.20%. Since there’s no way for us to calculate it with complete accuracy, we will use 0.90% for now (based on my 0.65 ratio formula of the 5-year daily TIPS yield) until the U.S. Department of Treasury releases what the new fixed rate will be on October 30, 2025.

Total rate = Fixed rate + 2 x Semiannual inflation rate + (Semiannual inflation rate X Fixed rate)

Total rate = 0.009 + 2 x 0.0156 + (0.0156 x 0.009)

Total rate = 4.03%

This means that starting in November 2025, new I Bonds will earn a slightly higher rate of about 4.03% (if my fixed rate guess is right).

Ninja Update 10/30/25: The fixed rate was just announced at 0.90%, which is down 20 basis points from the previous rate of 1.10%. Therefore, the total rate starting in November is indeed 4.03%.

Revised Total Rate Calculation = 0.009 + 2 x 0.0156 + (0.0156 x 0.009) = 4.03%

That signals to us that inflation has increased modestly and haven’t spiked the way that it did for the past few years, which is a good for consumers, but not so great for I Bonds.

What if I buy I Bonds before the rate change?

If you buy I Bonds between May 2025 and October 2025, you’ll be guaranteed a total rate of 3.98% for the next six months (based on the previous six months formula).

After that time period, your total rate is estimated to be 4.03% for the following six months. Assuming no change in the inflation data, then in terms of the absolute worse-case scenario, where you:

- buy I Bonds on or before October 30, 2025 (I Bonds take one business day to process)

- sell the I Bond on October 1, 2026 (hold the I Bond for the minimum 12 months and incur a three-month interest penalty)

You’ll earn a 3.33% annualized return for an 11-month holding period.

You may be asking why 11 months and not 12 months. It’s because in this scenario, you bought the I Bond at the end of October. Even though you only held the I Bond for a couple of days that month, you earn the entire month’s worth of interest. It’s a near little trick to buy at the end of a month and gain the entire month’s interest.

If you decide not to sell the I Bonds immediately on the 12th month, you’ll earn a 4.01% return instead during this period and will absorb the three-month interest penalty at the prevailing future rate.

Should I buy I Bonds now?

For the past few years, buying I Bonds was unquestionably the best option to grow your savings. You were earning returns similar to the stock market, but without any investment risk. That’s not the case anymore. I Bond rates have plateaued and they’re now offering smaller returns compared to other safe alternatives.

For instance, this savings account at SoFi offers an uncapped 4.30% APY with no minimum balance and no monthly fees (and a $325 sign-up bonus). In most cases, it doesn’t make sense to buy additional I Bonds right now when you can get a higher rate with no minimum holding period or early withdrawal penalty.

That’s what I’ve decided to do with my savings. If inflation rears its ugly head again and the rate for I Bonds increases significantly, I can withdraw my funds from my savings account at any time and buy more bonds.

However, there are some instances where buying I Bonds would make sense. For example, if you’re in a high tax bracket, you may want to defer paying income taxes on the interest you’d earn from a savings account.

How to Buy I Bonds

You used to be able to buy savings bonds by simply walking into a bank, but that’s not the case anymore. The government no longer issue bonds in paper form (besides tax refunds – more on that below), you can only buy them in electronic form.

You can buy up to $10,000 in I Bonds each calendar year through an electronic TreasuryDirect account. Open an account at TreasuryDirect.gov to do so. The minimum purchase amount is $25.

The $10,000 limit is per person, not per household. In other words, a couple can buy a total of $20,000 in I Bonds per year. A family with children can buy another $10,000 per child as long as they have a Social Security Number.

Additionally, you can buy an extra $5,000 in paper I Bonds if you have a tax refund when you file your federal income tax return. Tax software like TurboTax will offer you this option if you’re due a refund. If you do your taxes by hand, you need to complete IRS Form 8888.

The minimum purchase amount is $50 when buying through a tax refund (Paper I Bonds come in denominations of $50, $100, $200, $500, and $1,000).

Most people don’t get a tax refund of $5,000 – at least not if you’re doing your taxes right.

In instances like this where you want to buy more I Bonds and therefore want a bigger tax refund, a strategy you can use is to purposely pay more in taxes throughout the year than you actually owe.

Ninja Note: If you want to purchase more than the $10,000 annual limit, I wrote a detailed post on all the ways to buy more I Bonds.

The Bottom Line

Personally, between my wife and I, we bought $60,000 worth of I Bonds over the past few years, and the blended rate of return has been phenomenal. We started buying when I Bonds were at 7.12%, bought more when I Bonds peaked at 9.62% in the following six months, and the rate was 6.89% the last time we purchased them.

Considering how ultra-safe I Bonds are as an savings option, the blended rate was too good to pass up.

Although I don’t have plans to purchase more I Bonds for the reasons I explained in this post. Instead, I parked the rest of my savings in the SoFi Checking & Savings account.

I also keep a small amount of money outside of real estate and stock investments directed towards chasing the best bank bonuses, which has been a very lucrative side hustle.

But I strongly recommend creating an adequate emergency fund first. Save the money in a high-yield savings account before exploring others ways to make your money work harder for you.

Finally, I want to thank all my readers who have chimed in on this topic and supported the site. This article took hundreds of hours to research, write, and maintain over the past three years, but I’m so happy how much it has helped people!

Thanks, very informative. I am trying to work out exactly how the USG determines the variable rate using the CPI-U publication. https://www.bls.gov/news.release/cpi.t01.htm

This table lists indexes for Sep 23, Aug 24, and Sep 24. Your example uses different months, and it isn’t clear to me how that related to what I see on the BLS web site. It appears the “semi-annual” rate refers to the rate for the six month periods (May-Nov, Nov-May) used to set the variable rate. I can derive an annual rate from the BLS table and divide that by half, but that is probably not the rate used for I-Bonds, unless it happens to align with the May-November range. Is there a different source for those monthly numbers?

You’re welcome! I’m glad you found it helpful.

Regarding your question, if you look at the table I have under the subheading “November 2024 – April 2024 I Bond Rates”, you’ll see I listed the CPI-U numbers for each month (the row labeled “Inflation index”). Those are the same numbers you’ll find in the U.S. Bureau of Labor Statistics link you provided. For example, I have 307.789 for September 2023, which is the same number you found in that link for September 2023. The BLS site only shows the previous two months and the numbers from the same months of last year for comparison purposes. My table lists each data for the most recent 12 months. Does that help?

I thought this was an excellent article on I Bonds. Thank you.

Thanks Kris! I appreciate the kudos!

I appreciate the time and effort you put into this page. I refer to it often. I have a little tip for any novice and budget restricted investors like myself. Nothing to do with rates. I buy many small bonds totaling $10k max for the year. That way, if I am in an urgent need of money after the first year, I don’t have to take out the whole amount. I am able to take out as little as $500 and only have the penalty on that small amount.

Thanks again for making sense of Ibonds.

Thanks for the kudos, Susieq! And that’s excellent advice to create a flexible way to redeem I Bonds via smaller purchases!

Thanks for this page, it has served me well over the last few years.

I noticed your table under “Why didn’t you recommend I Bonds before?” has a mistake on the top line. You seem to have cannibalized the May23-Oct23 line with a partial replacement using Nov23-April24 numbers, and doubled the variable semi-annual rate.

May23-Oct23 should show Fixed rate of 0.9%, variable rate of 1.69%, and composite of 4.3%.

Nov23-April24 should show Fixed rate of 1.30%, variable rate of 1.97%, and composite of 5.27%

Also, your equation for Nov23-Apr24 in the section for that period’s bond rate shows:

Total rate = 0.009 + 2 x 0.0197 + (0.0197 x 0.013)

Total rate = 5.27%

The first Total rate line should not have 0.009, it should have 0.013 in the first parameter.

I got a bit confused trying to determine what to do going forward due to these typos.

Nonetheless, thanks for this page, it’s been great!

Thank you, AC! You’re totally right – some numbers were cannibalized from the multiple updates and have been fixed now. I appreciate readers looking out to ensure accuracy.

Glad to hear this page has been helpful for you over the years. I’ll try to improve my copy and paste skills for the next round of updates 🙂

I appreciate the post.

Does this make sense to you as a long term strategy for I-bonds?

Instead of buying i bonds when the total return is high, buy them when the fixed return is high. And hold the ones with the highest fixed return because over time they will beat inflation.

Since we can’t know what is a high return or when we will get a high variable rate, we can create a bond ladder by buying some bonds every 6 months.

Then, when it makes sense, we sell the bonds with the lowest fixed rates and hold the ones with high rates.

Some people are holding Ninfa with fixed rates over 1 percent.

Question: If buying iBonds for a solo 401k retirement trust, using the trust’s EIN, are we limited to $10,000? Even though the trust has both husband and wife? Thanks, very informative post.

Medora, in a legal sense, a Trust is an “individual”. Therefore, you can only open one account per Trust. Theoretically, a trust can be set up for 1 to infinite people. I posted another comment to note that each individual and each trust can have their own Treasury Direct account, therefore $10,000 per account can be bought each year.

The trust is still limited to 10K purchase

Great write up! I have purchased 2 Ibonds, both for $10,000. First purchase was October 2021, then second one in Jan 2022. I have been debating the best time to sell/redeem these Ibonds and place these funds either into a high yield savings or my brokerage account. I assume it would be best to hang in for an additional 3 months at the lower rate, given the 3 month penalty for a withdrawal prior to 5 years. I look forward to your input or comments from the group. Thanks

Thanks Troy for the compliment! Regarding when the best time to redeem I Bonds is:

Since it’s the most recent three months of interest that is taken out if you redeem I Bonds held less than five years, I would wait until January 1, 2024 to withdraw bonds purchased in October (regardless of which year you bought them). That’s because your six months of 6.48% interest finishes in September 2023. Your three-month penalty period takes up October, November, and December at the lower rate.

I would wait until October 1, 2023 to withdraw bonds purchased in January (regardless of which year you bought them). The 6.48% interest finishes in June 2023 and the three-month penalty period takes up July, August, and September.

Hi John…LOVE this page. Thanks for keeping it updated. A question for you:

Let’s say I own a 10K iBond purchased in December of 2021. I’ve owned it for more than a year and thus can sell it but must take a penalty of losing 3-mo of interest. If (because of the lower rate that is coming on May 1) I decide I want to get out of the iBond, I can either get out immediately (say, on 5/1) and lose 3 months of 6.82% interest, or wait 3 months (on 8/1) and lose 3 months of 3.13% interest. (Ignoring compounding for the moment, 3 months of 6.82% interest is about $172, whereas 3 months of 3.13% interest is $71.)

Thus, it would appear that by delaying getting out of the iBond for 3 months, the penalty for getting out is reduced by about $100. Sounds reasonable…

BUT…with current 3-month CD’s paying about 5%, another way to look at this (I think?) is to realize that if I get out on 5/1, I can put the total proceeds of my sale (10K+) into a 3-mo 5% CD which (again ignoring compounding) would result in income of $126 (10K at 5% for a year, is $500, or $42 per month…or for 3 months, I’d earn $126…which subtracted from the $171 penalty I took by getting out early leaves me just down ($171 – $126) $45! I’ve reduced the effective penalty by immediately putting the proceeds of the sale to work.

So, a big difference (to me) is that if I get out early (5/1) I can put the proceeds immediately to work earning some real money, whereas the person who stays in the iBond for 3 months extra just to get the lesser penalty is missing the opportunity to have the whole principal working for you earning a much higher rate during those same 3 months.

Does this sound reasonable or am I missing something? I know I made a lot of assumptions and a bit of rounding, but I just feel that’s it’s not quite proper to just say waiting an extra 3 months at the lower rate to get out lessens your penalty…because while your penalty is indeed lessened by about $100, in doing so, you’re giving up the opportunity to utilize the full principal earning a much better rate for those same 3 months.

Reasonable?

Hi Ken – thanks for the compliments! It takes quite a bit of time to update this, but I’m glad people find it useful.

Your analysis is reasonable and logical for the scenario you described. Depending on what state you live and your income level, I’d also consider that interest earned on I Bonds is exempt from state and local taxes and you can defer federal income tax on the accrued interest for up to 30 years.

So the “effective” penalty could be worse than your forecast.

Thanks for the quick reply John. I’ve been doing some more figuring just for fun, and the value of my possible approach (of getting out early on May 1 when the rates drop down, and using the proceeds to earn a much better yield (using MM or CDs) during the next 3 months when others may be earning a lesser yield by staying in the iBond to minimize the penalty) is pretty much totally dependent on the CD or MM interest rates available at the time of getting out. As a friend of mine will often remind me, you have to get out your speadsheet and do the numbers!

I purchased some Series I bonds in May 2022 when the announced interest rate was 9.62%. However, when I checked the composite interest rate published on the treasury website – (https://www.treasurydirect.gov/savings-bonds/i-bonds/i-bonds-interest-rates/), I see 6.48%. Did they change the rate from 9.62% to 6.48% for May 2022 to October 2022?

I checked my account and the interest in my account amounts to 3.2% from May to now.

Where did the 9.62% go?

The website shows your actual value to include the 3 month penalty. The first 6 months earned 4.81% (9.62% APY) followed by 6 months at 3.245% (6.49% APY) minus 3 months for early withdrawal. If you bought a $10k I-bond in May 2022, the balance shown this month should be $10,651. In July it would be $10,821. That is the actual cash value and already includes the 3 month penalty.

Very informative! I’ve purchased multiple i bonds over the past 16 months for me and the family and have been trying to understand the various value accruals and current shown balances. You pointing out the values shown are cash out rates with 3 month penalty makes a lot of sense.

From my understanding, as long as you wait until the first of the next month, that month will then count as one of your months (interest earned). I’ve moved to 4-8-17 week treasury bills vs I-Bonds since January 23, last I-bond purchase was Oct 22. I’ll likely start pulling my older I-bonds in early June or July if new rates are sub ~3.5% and T-Bills are still 4.5% or higher. (Whenever I reach the 3 months of lower new rate). Worth paying the penalty to move on into something higher yielding.

Can anyone explain the third part of the interest rate calculation — where we multiply the two rates (semiannual inflation rate X fixed rate). What are we/they accounting for here? The interest on the interest earned in that period? or?

Thanks

I don’t think it’s the interest on the interest. It’s some sort of calculation that marginally boosts the composite rate. Instead of 6.88% for the November 2022 cycle, it’s 6.89% thanks to the third part of the interest rate calculation:

Total rate = Fixed rate + 2 x Semiannual inflation rate + (Semiannual inflation rate X Fixed rate)

[0.0040 + (2 x 0.0324) + (0.0040 x 0.0324)]

Gives a composite rate of [0.0040 + 0.0648 + 0.0001296]

Adding the parts gives 0.0689296

Thanks for the excellent info. I have been buying these for a while but one thing I never understood is about cashing them. If you cash between the two annual payment dates (assuming a 5 year or older bond) do you get pro rata interest for the partial period? or should you always try to cash the day after a payment?

You get the pro rata interest. Although interest is compounded semiannually, it’s earned on a monthly basis.

Can a husband and wife buy $20,000 in i bonds using one treasury direct account or does each have to have their own?

Each person needs to have their own TreasuryDirect account.

I have one account and buy for me and wife using the “gift” option

Great article! The iBonds can be confusing.

You can also open an account for Trusts. Each account can have $10,000 contribution per year. In my case have four, so can invest up to $40,000 per year in iBonds:

1. In my name

2. In wife’s name

3. In my personal trust

4. In joint trust

We could even open a trust just in my wife’s name and have a 5th account; or theoretically have multiple trusts. The challenge is that creating a trust takes time and money ($1500-$2000 in our case) so the driver is your personal financial situation — in other words, don’t create a trust just for iBond account :-).

Do note: You can use the same social security number for different accounts (e.g. I use my SS# for personal account and my personal trust account). However, each account must have a unique ID and password.

If I purchased $5000 in i bonds in May, (thank you for the heads up!) I still could purchase another $5000 this year. That being said, is the rate announcement made with enough lead time to either hold off till November to buy at a new rate (hopefully higher) or purchase another $5000 at the 9.62 rate? Thoughts? AND THANK YOU!

You’re welcome!

There’s a slight lead time that allows you to plan appropriately, but if I were you, I’d probably buy another $5,000 now. You’ll lock in the 9.62% for six months and then whatever the new rate is. If you buy at the start of the new rate, even if it’s higher, the next set of six months may be lower. Taking a guaranteed high rate vs gambling for a unknown May 2023 rate is a no brainer for me. You can always buy more next year.

My husband purchased $10,000 under our company name to give us a third opportunity for the bonds. When he did it he made a clerical error on the bank account number. We had to send via certified mail the correct information. We received an email that it was received but that it could take up to 13 weeks for the request to be processed. Should we go ahead and purchase another 10,000 shares since it could be after the 1st of the year before the correction will be made?

I didn’t see an answer to the question about whether the interest compounds?

I Bonds earn interest each month and the interest is compounded semiannually (every six months).

What happens if the CPI-U declines from June to Sept? How can you say that the 3.06% change from March to June will be a floor? We already know that the CPI-U declined from a June reading of 296.311 to a July reading of 296.276. And inflation could possibly decline each of the next two reports. Or if there is now change period to period, than the variable rate could hypothetically be zero. Thoughts?

Good catch. I wasn’t expecting month-to-month inflation to stagnate for the next few months, but as you pointed out, CPI-U declined slightly in July.

We’re getting close to knowing what revised rate will be. I’ll update the post – thanks for mentioning this!

Do you know why it is that when I add up the monthly changes in the inflation rate for the current period I come up with 4.72%, not 4.81%?

Sorry for not seeing this earlier. Can you tell me what months are you adding up?

Thanks Carl, I agree with you.

Would it be prudent to buy an I bond through Roth IRA account? Can it be held in the Roth IRA account?

I bonds can only be held at Treasury Direct or paper bonds via tax refund.

Someone was telling me in a rather lengthy and somewhat wordy fashion to go ahead and buy my 10K worth of i-bonds in April. Said I’d be better off folding the old rate with the May rate.

At some point during our discourse i said i would cash in at 15 months taking the withdrawal penalty into consideration.

Keep in mind the three-month penalty takes the most recent three-month period. So if you did lock in the May 2022 rate, you’d maintain all six months of 9.62% rate, all six months of the upcoming November 2022 rate, and give up three months of whatever the May 2023 rate comes out to.

Married couple here filing jointly with two children, one child 22 other 25.

If we want to go forth to the max, how many I bonds $10k could be acquired three or four and do we all need to acquire our own accounts?

If you’re a married couple with two children, you can buy $10k per SSN. You and your spouse will need to open a separate account to buy your own bonds at the $10k limit.

If your children are under 18, you can open a custodial account to buy bonds in their name. Doing so will indicate it’s a irrevocable gift to the children though. Here’s a post with a section specifically detailing the purchasing of bonds for kids.

https://themoneyninja.com/how-to-buy-more-i-bonds/#3_Buy_I_Bonds_Through_Your_Kids

Hi,

Great article. My husband and I maxed out and bought $10000 each month in November and December 2021 and again $10,000 each month in January and February 2022.

My question is a person or joint filers have a choice of paying federal tax now or later when bond is cashed. There is no state or local tax on the total composite gain. Does it make more sense to pay taxes now (if it doesn’t change tax bracket) before taxes eventually go higher? I’m feeling like that is the right thing to do and save a major tax bill later. I realize once you do it a certain way, for the bond’s life, you are committed to whichever way you decided. I’m just trying to plan for 2022 taxes..lol. Thanks.

Hi Kris, thank you!

Regarding your question, reporting interest income each year instead of deferring it could be a good move for someone with little or no taxable income and expect it to be significant higher in the future.

I’m not sure what tax bracket you’re in or expect to be in later so I can’t advise a straightforward yes or no. It’s also hard to predict whether the tax brackets will go higher or lower.

This strategy is clearer in specific scenarios, like if the savings bonds are held in a child’s name. They are most likely paying taxes at a lower rate today than in the future as the bond matures.

I missed the April 30, 2022 deadline. It is now May 2nd. Should I buy I bonds now or wait until the end of the month.

There’s no reason to wait until the end of the month unless you’re earning interest on the money you intend to invest in i bonds, and it’s worth waiting most of the month to continue to get that interest. This is a highly unlikely scenario.

Awesome of you to share your knowledge and put your time as well to do it !

I wish I had known about this I-Bond 20 years ago. This thing appears to be like one’s own Social Security system, or an augment to SS, at retirement.

If I understand it correctly, if my wife and I were to put 20k a year into it for 20-25 years then compounded at, or close to, retirement we’ll have a pretty sizeable, if not double, amount to withdraw from for along time thereafter. So, SS+ I-Bond draw.

I’ve just opened an account with Treasury Direct. It is letting me add another registration where I was able to add my wife’s SS# too. Not sure at this point if I’ll be able to add 10k for each registration, or if my wife needs her own account. Will find out soon 🙂

Thanks Much for your site. Its worth sharing and recommending !!

If the Fed decides to change the current fixed rate of 0%, when could that take place?

At any time or only once a year?

It can happen twice a year, at the same time they announce the variable rate portion of the bonds.

Can I buy Savings I bonds for spouse and myself for $10000 each for this calendar year and also each of us buy $10000 as gift to one another and deliver it next year to maximize the gain and avoid yearly limit?

Yes, that’s a potential strategy! The only caveat is that the gift has to be “received” in a different year.

For example, John and Jane are a married couple and each of them has already bought $10,000 in I Bonds for 2022. John can buy an additional $10,000 (or whatever amount) during 2022 with the gift being fully executed (“received”) to Jane in 2023. Since John bought the I Bonds in 2022, the savings bonds will begin accruing interest and counting down the 12-month lock-up period at the time of purchase.

Keep in mind if Jane elects to receive the bonds in 2023, she has to deduct that bond amount against her annual limit.

So, Jane (and John) can defer receiving/execution of their gifts to 2024 and buy another 10k each in their own accounts on 1/1/23?

i.e. have a total of 40k begin to earn the current rate of interest right now and add another 20k in Jan 2023?

That’s correct, but I wouldn’t perpetually stack more and more I Bonds – maybe a few years at most.

Because what if in the next several years, the U.S. experiences significantly lower inflation levels? The variable rate would go down by the same margin. In that situation, you don’t want years of bonds that you need to unload $10,000 at a time.

can you gift 10,000 to yourself for the next year?

No, you can’t name yourself as the owner of a gift. You can be a beneficiary, but you cannot be the primary owner or secondary owner.

One strategy if you have a significant other is to “gift” each other I Bonds. Wait until interest rates drop and the two of you stop buying I Bonds to take delivery of the gifts. The gift bonds earn interest starting on the day of purchase and will have aged enough to cash out immediately if desired.

If the new rate next year is still high, my wife and I will buy more and keep the gifts in the gift box. If the interest rate drops, we’ll skip the purchase, deliver the gifts, and cash them out.

I have a custodial savings account for a grandson. Can I remove money from that account and purchase an I Bond in his name? He is nine years old.

Yes to both. You can withdraw money from a custodial account as long as the funds go toward the benefit of the grandson. You can also purchase savings bonds under the name of the grandson.

I bought two $5000.00 I bonds April of 2009

One for me and one for my wife

What are they worth

What are they earning

Should I sell them and buy new I bonds

Do I have to sell them after thirty years of holding

They are paper bonds should I set them up differently

I intend to get more now, today is Friday April 29, 2022, should I wait until later in May to get them as the interest amount will be the same

You can go here to calculate the value of your paper bonds. They’re earning the same variable rate as every active I Bond, currently at 9.62%.

You don’t need to sell them as they’re still earning interest; they will just no longer accrue additional interest after 30 years. You can (and probably should) buy more this year to take advantage of this high rate of return. There’s no “set up” for paper bonds. To redeem them, go to your local bank.

Electronic I Bonds behave a bit differently – when bonds in a TreasuryDirect account stop earning interest, they’re automatically cashed and the interest earned is reported to the IRS.

CORRECTION: There is a way to convert paper bonds to electronic bonds. It’s cumbersome, but worth it in our case. They electronic ones end up on the Treasury Direct website as a subaccount uner your main account. Google “I Bond Conversions” for details.

i couldn’t find a way to list beneficiary or TOD or anyway to pass along in case of death. did i miss something

You have to name a second owner. That second owner becomes the beneficiary if you should pass away. Each I Bond holding allows only one second owner or beneficiary but not both at the same time. This second owner or beneficiary must be a person, not a trust or a charity. If you’d like to leave your I Bonds to multiple people after you die, you must make separate purchases and name a different person for each I Bond.

Question if you both die in accident does the bonds go into probate or can you will them?